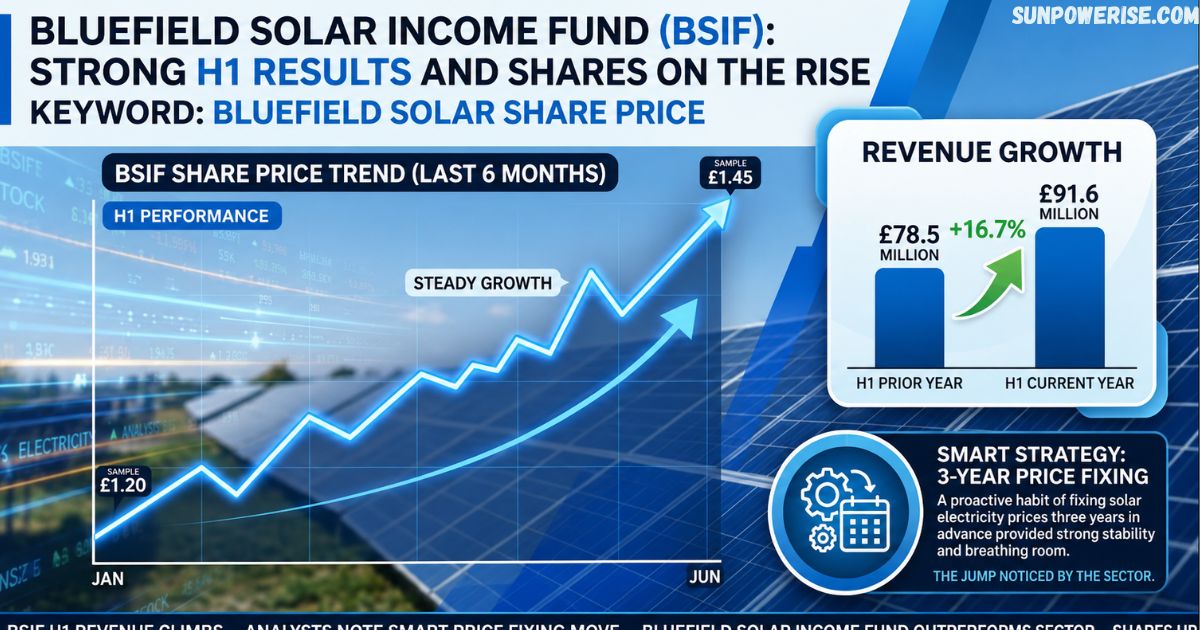

The bluefield solar share price sits against a backdrop of steady growth, and the first half of the year brought strong numbers worth talking about. Revenue climbed thanks to a smart habit of fixing prices three years in advance, a move that gave the company real breathing room. That single choice turned £78.5 million into £91.6 million, and anyone tracking the sector noticed the jump.

James Armstrong, the managing partner at Bluefield Partners, sat down for a chat on Proactive to walk through the details. He also works as one of the investment advisors guiding this fund, and his role as an investment advisor means he sees both the numbers and the story behind them.

Later, in a separate update, he returned to discuss phase two of that same program and eventually opened up about the strategic review the company launched.

Each appearance built on the last, layer by layer. I found that pattern genuinely useful for understanding how the share price story unfolded over time.

Bluefield Solar Share Price Discount to NAV

The share price tells one story, but the results tell another, and that disconnect is the heart of this whole discussion. Bluefield Solar posted a record period, with strong performance across the full year, yet the market barely reacted. I remember checking the numbers myself and feeling puzzled by how wide that gap had grown.

Strategic Price Fixing & Dividend Coverage

Much of the strength comes from a power fixing strategy that leans on long-term linked revenues tied to RPI, a setup built for steady income investors.

On top of that, fixing high prices for one to three years ahead locks in extra cash. Dividend cover sits at two times, even after debt amortisation and the electricity generators levy take their share.

Unprecedented 25% NAV Discount

Despite all this, the NAV, short for net asset value, sits well above the share price, creating a 25% discount that has lasted for three years, in fact, closer to three and a half years in some readings.

This is the first time in an 11-year history that shares have traded this low against fundamentals, and analysts like Benjamin Graham would call it a case of Mr Market losing its head.

Portfolio Resilience Amid Sector-Wide Pressures

The West Rum plant briefly went offline during the summer, handled by the distribution network operator, but it only cost around £1 million in losses, roughly 0.2 of a penny per share, so it barely moved the needle.

This plant covers 5% of the total capacity, and the wider portfolio stayed resilient. The real pressure came from the broader renewable sector, a sub-sector within long-dated infrastructure funds, where discounts hit almost every name.

Valuation Anomalies & Market Catalysts

Look at 104p share price against a £635m market cap, and you can see the fundamental basis for calling this undervalued.

A recent UK solar transaction of 500 megawatts, with similar asset types, closed at a valuation that would be accretive to NAV, based on real transactions in the open market comparison. That kind of catalyst rarely shows up so clearly in the investment company space.

High Yield Potential & Future Outlook

Investors buying now can lock in a yield near 8.5–8.6%, well above the historic premium this fund used to command over NAV, rather than trading below it.

The public market and the investment company market for infrastructure funds are both stuck in a persistent discount, a pattern seen since post-Christmas across the sector, and a forecast built on a proprietary pipeline still points to brighter days within roughly one year.

The Justification for Fair Value

Some readers ask why the 136p per share NAV figure matters so much. It simply shows fair value, and the current discount between that figure and the trading price is hard to justify.

Add in strong cash generation each quarter, plus a share price pressure environment gripping the whole sector, and shareholders like me start asking tough questions. Even the levy applied above 75 on power sales barely dents the bigger picture, since the fundamentals remain solid.

Share Buyback Program

Fixing a prolonged discount is never simple, and the team spent six to nine months working through options before acting. They called it a multi-faceted challenge, and honestly, that phrase fits well because there was no single fix.

What came out of that period were major initiatives designed to protect long-term value drivers, along with a large development pipeline built over a decade of steady work.

GLIL Partnership & Capital Reallocation

One piece was a strategic partnership with GLIL, a name tied to pooled local authority pension funds, allowing a sell-down of 50% of assets.

That single move created liquidity for shareholders, helped repay a short-term credit facility, and supported the wider development pipeline. It was, in my view, a sensible response to a genuinely tricky situation.

The £20 Million Share Buyback Initiative

The second piece, a board-approved share buyback program worth £20 million, was confirmed on 14th February. This buyback effort, funded through the same £20 million program, also strengthens overall liquidity across the balance sheet, and it runs in the open market, buying back shares directly.

The board plans to review it after another six to nine months. Calling it a brave response feels fair, since it shows real responsibility toward investors.

Rising Pressures & The Post-Christmas Dip

Before this, the discount widened sharply after the new year, even though every name across the sector had already been trading at a lower discount heading into Christmas.

Bluefield had actually held up better than peers during that stretch. Even so, the gap kept growing, and that pushed the board to act.

Record Fundamentals in a Decoupled Market

None of this points to a fundamental problem, quite the opposite. The fundamentals behind Bluefield Solar look as strong, or stronger, than at any point in its 12 years as a public IPO.

The goal now is simple: address the short-term discount issue while keeping the discount to NAV narrowing over time, hopefully sparking a re-rating.

Shareholder Consultation & Proactive Engagement

Separately, Bluefield Partners ran a long consultation, consulting closely with shareholders for months, with real focus after the 21st October update.

The fund carries an unparalleled track record and other attractive characteristics, including a sector-leading generation profile. Even so, the investment advisor and the boards of many investment companies agree that doing nothing was never an option.

Formal Strategic Review for Maximising Value

That thinking led straight to the formal strategic review and eventual formal sale process, both aimed at maximising value for owners.

It came down to three ways of protecting the business, addressing both the short-term picture and the three and a half years of pressure the shares had carried. In the end, it was a fantastic strategy, executed with genuine care.

Strategic Review and Formal Sale Process

James Armstrong put it plainly: the goal behind this whole move is unlocking longer-term value while also maximising shareholder value and building liquidity for investors in a short period of time.

It is a genuinely unique proposition put forward as part of the sale process, addressing the persistent discount to NAV head-on.

The Unitary Transaction

Rather than sell the operational portfolio alone, the plan bundles it with the development pipeline and the platform of businesses into one transaction, opening access to capital and different types of capital that would not usually chase operational assets on their own. That structure widens the pool of potential buyers considerably.

High-Quality UK Portfolio and Private Growth Potential

Buyers should find plenty to like: a high-quality, diversified operational portfolio that is firmly UK-focused, giving strong geographical focus, plus real growth potential tied to the wider platform.

There is also a chance to internalise the Bluefield group of companies, covering everything from development through to operations, especially for anyone taking the private route. A proven operational team and management team round out the picture, offering existing shareholders genuine routes to exit.

Looking ahead, the next steps rest with the financial advisors, who will handle market updates as the formal sale process continues. The board and advisors are working to keep things an efficient process, with shareholders expecting regular updates along the way.

Dividend Guidance

The Bluefield Solar share price reflects a business where management has reiterated its full-year dividend guidance of at least 8.8 pence per share, holding onto an 8% dividend yield.

The business has stayed genuinely cash generative over the past few years, and that shows up in strong dividend cover, among the highest dividends anywhere in the infrastructure space.

That confidence rests on index-linked regulated revenues, an effective power strategy, and a stable asset base. Put together, it forms a genuinely attractive dividend for potential shareholders thinking about buying in today.

FAQs

Is Bluefield Solar a good investment?

With strong dividend cover, steady cash generation, and shares trading at a rare NAV discount, many investors find it genuinely attractive today.

What do analysts predict for Bluefield Solar Share price?

Most views point toward the 136p per share NAV as fair value, with a re-rating expected if the strategic review and formal sale process succeed.

What is the target price for Bluefield Solar?

The widely referenced target sits near the NAV of 136p per share, based on recent UK solar transaction valuations for similar asset types.

What is the history of Bluefield Solar?

Bluefield Solar Income Fund has an 11-year history since its IPO, built on a proven operational team and a large development pipeline across the UK.

Who are Bluefield Solar’s main competitors?

Its closest peers sit within the same renewable sector and infrastructure funds space, facing similar NAV discount pressure across the investment company market.