When tracking the Foresight Solar share price, it is notable that the fund manager, Toby Virno, and the company’s chair, Tony Roper, both gave a refreshingly honest assessment of where things stood when first looking into the Foresight Solar Fund.

This is a billion-pound business that spans the UK and mainland Europe, and it stands among the UK’s biggest solar funds, holding a mix of solar farms and battery storage assets that push clean power into the grid.

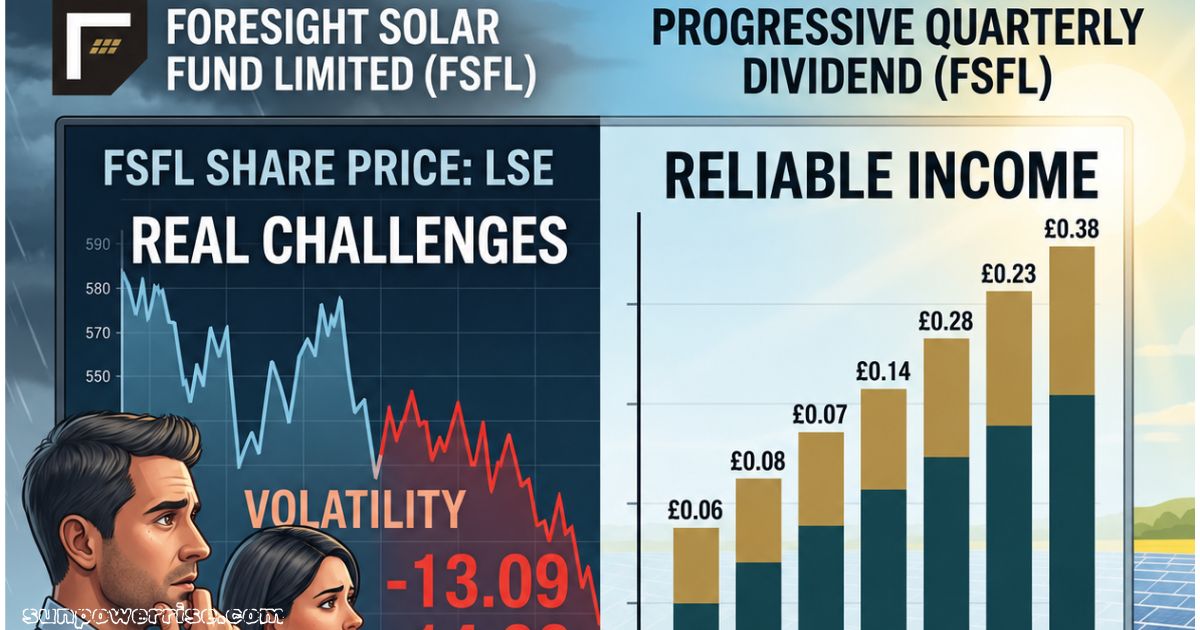

Investors watching the Foresight Solar share price of FSFL will know that despite real challenges, the fund still offers reliable income, with a progressive quarterly dividend that remains fully covered, a dividend currently yielding close to 12%.

All tied to a broader game plan built around transition, climate change mitigation, and a lower carbon economy, details laid out in the notice of AGM ahead of the meeting on the 3rd of June, where Foresight Solar’s performance and renewable energy strategy, along with enhanced capital value for shareholders, will be reviewed by the board and investors alike.

Portfolio Scale & Overview Of Foresight Solar Share Price

When evaluating the Foresight Solar share price, it helps to think of Foresight Solar’s portfolio as a sprawling network rather than a single site, because it stretches across the UK, Spain, and even Australia, blending operational assets with projects still under construction.

By the end of 2025, the operational portfolio had reached 994 megawatts, part of a wider total capacity close to two gigawatts once every project is finished, all backed by roughly a billion pounds of capital deployed across solar farms, battery storage assets, and mainland Europe sites feeding clean electricity into the grid.

Investment Objective & Strategy Pillars

What stands out to me about Foresight Solar’s approach is that it rests on four main pillars: income, growth, a geographically diverse portfolio, and operational excellence, all guided by specialist investment management from the Foresight Group, a real assets manager known for international scale and local networks.

Since its IPO, the fund has built a track record of a growing dividend and rising target payout, and over a decade it has beaten its own production forecasts in most years, a sign of genuine operational excellence and a dedicated portfolio team watching quality, availability, and value uplift closely.

Because solar sits among the cheapest and most reliable power sources, and because more countries are shifting toward green sources of energy to cut emissions, the fund’s proprietary development pipeline, spread across multiple markets with different support mechanisms and regulatory frameworks, gives its investment proposition a key strength.

Geographic diversification across varying levels of radiation, supporting steady income, stronger returns, and long-term success as projects move from development through construction into operations.

Business Model “Clean Energy Cycle”

The clean energy cycle is, in my view, one of the simplest ways to understand how Foresight Solar turns sunlight into money, because it follows four steps: find and buy opportunities, develop and build them, operate and enhance them, then either hold the assets for a cash yield or sell and recycle the proceeds back into new opportunities, forming a continuous loop.

In 2025, this business model generated £92.8 million, produced over 1,000 gigawatt hours of clean energy, and returned more than a quarter of a million pounds to local communities.

Financial Performance & NAV

Reading through Foresight Solar’s 2025 numbers, I noticed a challenging year told through two very different stories.

The core business performed well, with UK assets beating production expectations and enough cash to cover dividend payments, yet the financial markets were unkind, with net asset value slipping as safer investments looked more appealing once interest rates climbed.

Starting at 112.3p in 2024, NAV fell to 99.2 pence per share, a 99.2p figure confirmed in the Q1 NAV update and matching the prior Q4 position, a 14% drop driven by falling predictions for future power prices, weaker radiation, cheaper natural gas, a flood of new renewable projects, a seasonally weaker winter period, and a widening gap between market value and the fund’s true intrinsic worth, or paper value, per share.

Share Price Discount to NAV & AGM

The board of Foresight Solar has been upfront that FSFL shares have traded at more than a 10% discount to NAV throughout 2025, a gap driven by macroeconomic challenges across the whole renewable infrastructure sector, including higher interest rates, a volatile power price outlook, and an uncertain regulatory environment that has dampened investor sentiment.

Despite this, shareholder value has been supported by stable cash flows and strong operational performance, with the dividend 1.3 times covered in 2025 and 1.1 times dividend cover expected in 2026, all part of a fully covered dividend policy that reflects sound governance among listed renewable infrastructure investment companies.

At the AGM on the 3rd of June, shareholders will vote on resolutions to appoint directors and approve financial statements, alongside a discontinuation vote tied to the fund’s future, with strategic options and the AGM circular both aimed at protecting the share price.

Capital Recycling Strategy

Capital recycling sits at the cornerstone of Foresight Solar’s plan, and I find it a genuinely smart strategy: sell high by disposing of mature solar farms, then reinvest smart the proceeds into new projects still moving through construction, a process built to work sustainably over time.

This three-part strategy also leans on the development pipeline, now past 1,000 MW, alongside disciplined hedging of power prices to protect against swings.

While selective divestments and efficient recycling of capital extend the duration of long-term contracted revenues and contracted revenues, supporting modest capital appreciation as projects move into operations and de-risking continues.

Central to the portfolio mix and portfolio renewal is the UK, the fund’s home market and target market, where UK Contracts for Difference, known as CfDs, offer attractive revenue streams, and where active power price hedging together with balance sheet strengthening initiatives and reinvesting proceeds keep the cash flows and returns flowing, making this pipeline a genuine growth engine for future projects and cash.

Dividend & Income

Income-focused investors often ask me whether Foresight Solar’s dividend can hold up, and the answer lies in the numbers: an 8.1 pence per share dividend target, a fully covered payout yielding close to 12%, with dividend cover at 1.3 times for 2025 and 1.1 times projected for 2026.

Over a decade, FSFL has lifted its target payout by 35%, building a genuinely growing dividend from steady income, and recent policy changes from the UK government are not expected to disturb that dividend.

Environmental & Community Impact

Reflecting a positive operational performance that could impact the foresight solar share price, Foresight Solar’s 2025 results carry a real-world weight, generating enough clean energy to power roughly 380,000 homes across the UK for a full year. That same output kept close to 360,000 tons of carbon emissions out of the atmosphere.

Private Market Partnerships

Foresight Solar, with an eye on factors influencing the Foresight Solar share price, is exploring private market partnerships to support its investment program, with discussions still at an early stage and no certainty of outcome yet.

These potential arrangements could allow co-investment opportunities that speed up portfolio renewal and reinvestment, though the fund is careful not to over promise on the eventual outcome.

Q1 2026 Update

Looking ahead, investors tracking the Foresight Solar share price will note that UK government proposals aim to decouple electricity prices from natural gas prices, a shift driven partly by volatility tied to geopolitical conflicts in the Middle East.

Reassuringly, these policy changes are not expected to touch the dividend target or dividend cover, and Foresight Solar has promised further updates later this year.

FAQs

Is Foresight Solar Fund a good buy?

Foresight Solar Fund offers a fully covered dividend yielding close to 12%, but the share price trades at a 10% discount to NAV, so it depends on your appetite for short-term risk against long-term income.

Is Foresight Group a buy or sell?

As the specialist investment manager behind Foresight Solar, Foresight Group’s strength lies in steady operational excellence and international scale, making it a name investors watch closely rather than a simple buy or sell call.

What is the outlook for Foresight Solar Fund?

Despite a challenging 2025 with NAV falling to 99.2p, the capital recycling strategy and growing development pipeline point to a more promising long-term success.

How often does Foresight Solar pay dividends?

Foresight Solar pays a progressive quarterly dividend, currently targeting 8.1 pence per share, with dividend cover of 1.3 times in 2025.

Why is Foresight Solar share price trading below its NAV?

The share price discount stems from macroeconomic challenges like higher interest rates and investor sentiment, not from weak operational performance.